Putting cows on the front page since 1885.

Putting cows on the front page since 1885.

Financing equipment is a great tool to keep working capital in your hands. Loans and leases are both viable options, but what is the difference between the two, and which will work best for your operation?

Most people are familiar with a loan, but leasing is another way for customers to obtain the equipment they need to get back in the field. A lease is an agreement between the equipment owner (lessor) and a customer (lessee) to pay for the use of the equipment in the form of rental payments for a specific amount of time with an option to return or purchase the equipment at the end. At the end of the lease term, you then have the option to purchase the equipment you have been using.

An important term to understand when it comes to leasing is residual value, which is the value of the equipment at the end of the lease (and the stated purchase price that the lessee would pay should they choose to purchase the piece at the end of the lease). The residual value helps determine what payments will be. A higher residual means lower lease payments.

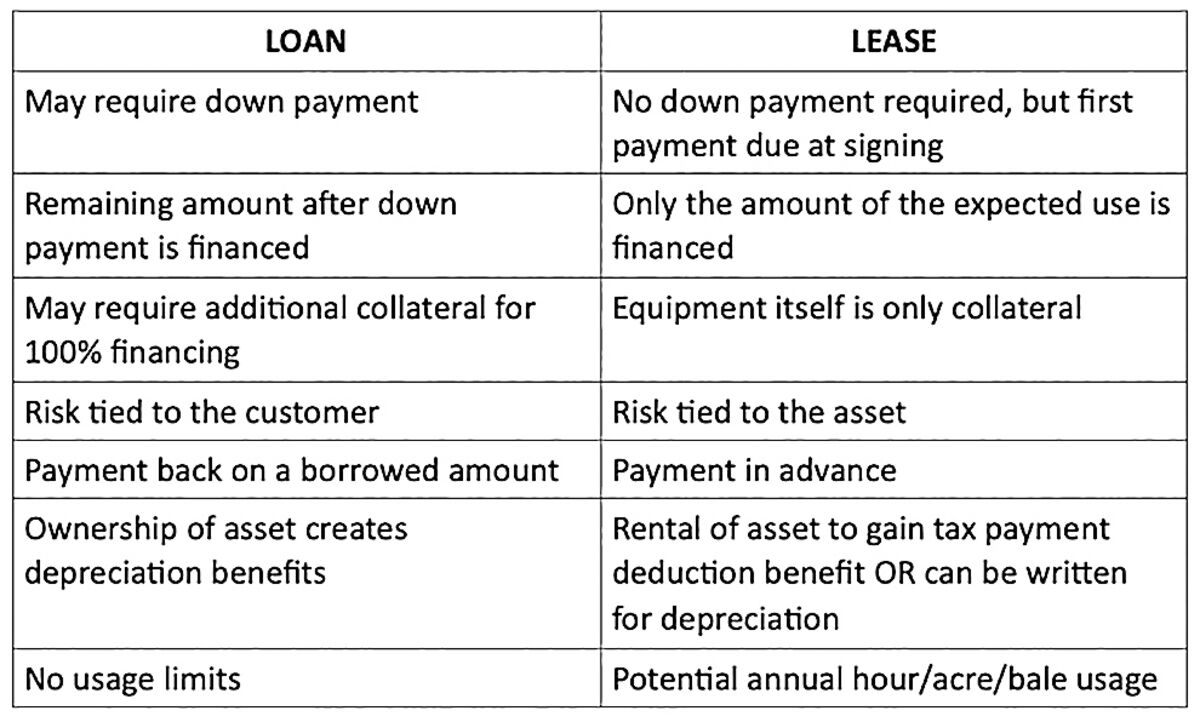

The top chart shows the differences between loans and leases.

Let's walk through an example:

A customer is looking to acquire a $100,000 tractor. He'd like to work with Farm Credit for a loan or lease and is comparing the two options. The bottom chart shows the difference between his two options.

In this case for leasing, the lessor or owner of the equipment would be Farm Credit. The lessee is the customer. The residual value of the tractor after 60 months of use is 51 percent ($51,000), which was determined by several factors including how many hours of use, term length, and what the customer wants to do at the end of the lease (walk away, renew the lease, or purchase the tractor). In this case, the customer planned to renew the lease or purchase the piece, and that new contract would work off the $51,000.

It is important to note that when leasing a piece of equipment, the customer is also responsible for all insurance, maintenance, taxes (if applicable), and all other costs of ownership (example: fuel).

Most customers are comfortable with a loan, but less familiar with leasing. Why would someone lease?

• Leases offer 100 percent financing, with no down payment required. However, the first payment is required at signing.

• Leasing can save money. Your payments accrue on a smaller balance, with the residual acting like a balloon payment at the end, rather than the full cost of the equipment. Talk to your lender for more specifics on this.

• Leasing helps preserve working capital for other purposes, as you are only paying for the portion used, rather than the full value of the piece.

• Cash flow can be improved since the flexibility of leasing allows for the payment schedule to be extremely customized.

• When leasing, equipment can be replaced faster to keep up with current technology, ease the difficulties of equipment obsolescence, and ensure access to reliable, low maintenance equipment with the newest options at all times.

• There is less ownership risk - the lessor bears the risk on the residual value (ex: equipment values are extremely high now, and if they fall, that is the lessor's problem, not the customer's).

• Leasing is a great tax management strategy. Payments can be deducted as operating expenses to lower taxes. Larger deductions over a shorter period accelerate the write-off.

• Leasing is also predictable expensing, rather than "one and done" with bonus depreciation and Section 179.

• Leasing is a great estate planning tool. Leased equipment is easily transitioned to the next generation at the end of the lease term.

Always consult with your CPA or tax professional to make sure you are choosing the best financing option for you and your business.

It is no secret that the current market for equipment is unlike it's ever been before. Availability is still an issue, although better than this time last year. Prices have certainly increased, and there are a number of other reasons customers site for caution with their equipment acquisitions. Let's assume that most pieces are 20 percent more than they were two years ago. On a big purchase, like a forage harvester, that is extremely significant. A lease can be much more palatable, especially with high residual, thus creating lower lease payments.

Reader Comments(0)